- English (UK)

February 2026 UK GDP: Strong Data Masks Mounting Downside Risks

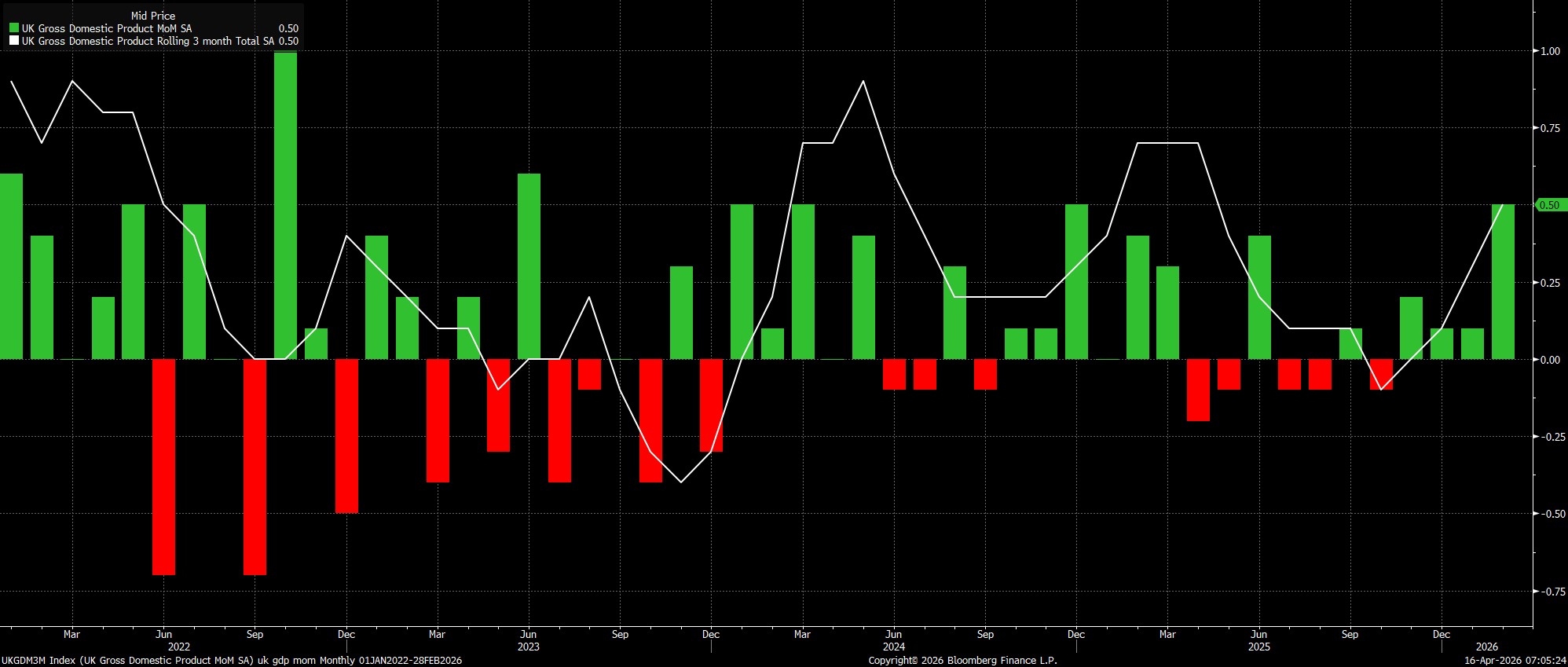

The economy grew by 0.5% MoM in February, the fastest monthly pace of expansion seen since December 2024. In turn, this dragged the rolling 3-month pace of growth higher, also to 0.5% 3Mo3M, the fastest such pace since last April.

In fact, growth was rather broad-based during the month. Construction output surged 1.0% MoM, rebounding from an upwardly-revised 0.5% MoM in January, while services output grew by 0.5% MoM, also faster than expected, and the fourth consecutive monthly expansion.

In any case, the February GDP report is, at this point, incredibly stale, with the economic backdrop having moved on considerably since the period in question. Conflict in the Middle East broke out at the beginning of March, subsequently triggering a significant surge in commodity prices which, in turn, will not only bring with it higher headline inflation, but will likely also act as a major negative demand shock, denting consumer spending and business investment alike.

With this in mind, today's data shan't materially impact the likely BoE policy path. For now, the MPC are likely to remain on hold, adopting a 'wait and see' approach to policymaking as economic uncertainty remains elevated, while both the magnitude, and the duration, of the energy price shock presently remain unknown. That said, there remains a path to one, or two, rate cuts still being delivered in the second half of the year, with the potential for second-round inflationary effects very limited indeed, meaning that the energy price shock should trigger more of a short-lived 'hump' in headline inflation, with limited spill-over into core metrics, as opposed to presenting risks of persistent price pressures as developed after the last major energy shock, in 2022. All that said, next week's jobs, inflation, retail sales, and PMI surveys are all likely to be considerably more instructive when it comes to gaming out the MPC's likely policy actions, compared to the stale growth figures just released.

Still, risks to the growth outlook quite clearly tilt to the downside at this moment in time. The UK economy was already on a very fragile and shaky footing before conflict broke out, with said conflict obviously bringing with it further growth headwinds. In many respects, taking both this, and the already-anaemic economic momentum seen pre-conflict, the risk of recession in the UK seems under-priced.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.